There is no shortage of information on the Internet about how to start a solo or very small law practice, perhaps because there are too many recent law graduates unable to find firm jobs and so become “suddenly solo” young lawyers, and I don’t mean to add more general advice to that big pile. I’ve never been a solo practitioner; I am, however, responsible for my own cases and accountable for my own revenues and expenses, and I have also seen my fair share of other lawyers who struck out to be solos and then, well, struck out.

In the big picture, I think Jordan Rushie’s reality-check about starting a solo practice and this interview on The Girl’s Guide To Law School give some of the best single-article advice on the internet about running a practice. New lawyers with their own practice, if nothing else, should repeat to themselves “most malpractice and disciplinary actions result from a lack of follow-up and follow-through” 108 times daily, like a religious mantra, until the importance of process sinks in. (I’ve previously written my thoughts on marketing for young lawyers, and how litigators can improve their skills.)

Carloyn Elefant recently ignited another debate over solo practice with an anonymous guest post by a lawyer describing how his experiment in solo practice failed. Scott Greenfield challenges the author’s mistaken “expectation that he would not only be able to create a viable practice out of nothing, but that it would allow him work/life balance.” Sam Glover similarly notes that there is no free time in the first few years of a solo practice, there is merely more time for marketing and networking.

There was, in my opinion, another fundamental problem with the anonymous poster’s experiment. His business model misunderstood the nature of contingent fee litigation:

I planned to practice criminal defense, immigration, civil rights (police and corrections misconduct), and consumer law (debt defense and FDCPA). My essential plan was to finance contingency civil rights work with revenue from flat-fee criminal, immigration, and consumer work and contingency FDCPA work.

(Emphasis mine.) Before I practiced contingent fee litigation, and perhaps in the first few years, I would have thought this contingency-and-fixed business model for a solo or small firm made sense. It looks like a good way to hedge bets: on the one hand the solo would have the regular income from the hourly and flat fee work, and on the other hand, have the irregular but potentially more lucrative income from the contingency fee work. I still hear lawyers talking about setting up their practice this way, mixing everything from family law to small business with personal injury or civil rights work.

Adding to the apparent sense of this business plan, there’s a handful of prominent lawyers in every city thriving on this model, usually (for reasons that will have to wait for another post) by mixing criminal defense along with catastrophic injury and wrongful death. Don’t be fooled. These success stories are the exception, not the rule, and they succeed because they have two things most solos likely don’t: a large referral network and big war chest. Their business model, however, does not scale down to the average solo practitioner’s size. Let’s review a little math to see why not.

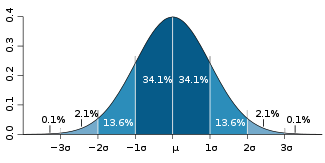

When people think of probabilities, they think of the bell curve, a.k.a. the “normal” distribution. As a refresher on statistics, in a “normal” distribution of numerical values, about 68 of the values are within 1 standard deviation of the mean, the dark blue area. 95% of the values are within 2 standard deviations of the mean, the combined dark blue and medium blue areas. More than 99% of the values are within 3 standard deviations of the mean, the combined blue areas.

As a refresher on statistics, in a “normal” distribution of numerical values, about 68 of the values are within 1 standard deviation of the mean, the dark blue area. 95% of the values are within 2 standard deviations of the mean, the combined dark blue and medium blue areas. More than 99% of the values are within 3 standard deviations of the mean, the combined blue areas.

Assume the middle represents an “average” income for a hypothetical criminal defense or family law or other hourly, flat or fixed fee lawyer. Ask that hypothetical lawyer, “how much do you think you’ll earn if you have three bad years in a row?” and “how much if you have three good years in a row?” and they will probably tell you the numbers at the edges of the dark blue, one standard deviation from the mean, covering 68% of the possible incomes they could have.

Replace the words “bad” and “good” with “terrible” and “amazing” and they’ll probably give you the numbers at the medium blue edges, two standard deviations from the mean. Use “worst” and “best” and they’ll give you the numbers at the edges of the light blue, three standard deviations from the mean. The “normal” distribution is so common, and so heavily ingrained in our culture, it’s hard to think of probabilities in other terms.

That’s usually fine for planning law firm revenues, and it’s applicable to most contingency fee firms, too. If you look at the annual revenues at the trial lawyer firms’ in any given city, they’ll usually follow a nice bell curve pattern over the years, with most years’ revenue within one standard deviation of their average annual revenue, and few years that are either earth-shatteringly good or sharply unprofitable.

But the devil is in the details: an individual contingency fee case is nothing like a paying client: contingency fee cases eat money in litigation costs for years before they bring a dime in, and often terminate with a total loss.

The reason the trial lawyer firms’ revenue follows such nice probabilities is because they have hundreds of cases, many filed years ago and thus ripe for settlement or judgment in the current year. For their portfolios, the law of large numbers applies: so long as the lawyer has done a good job of selecting and prosecuting cases — i.e., so that they turn a profit on cases more often than they don’t — they’ll rarely end up in the situation where they have a string of major losses without any victories to offset the expenses.

The solo practitioner, however, won’t have dozens of contingency fee cases about to reach a settlement or judgment each year. When they start out, they’ll likely have no settlements of any size for years, but the economic problem goes deeper than that. Even if they have a couple cases when they are, and even if they have a significant intake of worthwhile contingent fee cases, they’ll be too busy with the hourly work — which they need to stay afloat and to fund the contingency fee cases — to accept that many contingency cases. In all odds, a typical solo practitioner with a hybrid contingent / billable portfolio will be able to count their cases ripe for settlement in a given year on one hand.

The profit/loss a solo practitioner has on contingency cases, then, won’t follow “normal” distribution and the bell curve in each year — or even every two or three years — because they won’t have enough cases to smooth out the large losses. Instead, their profit/loss will follow a Poisson distribution. Sometimes they’ll have a couple winners in a row, sometimes they’ll have a couple winners that just happen to cover the costs of the cases still in suit. Sometimes they’ll have several losses in a row — while they still have to fund the contingency cases that remain in suit, and fund any new cases that come in the door.

Thus, the annual profit of a solo practice funding contingency cases through hourly work as a whole won’t follow a normal distribution, it will follow a Taleb distribution, so named for Fooled by Randomness and Black Swan author Nassim Taleb: it will appear at times deceptively low-risk with steady returns, but will experience periodic catastrophic drawdowns.

Everything will look great for the solo practitioner, as he or she slowly builds up a portfolio of hourly work and contingency fee cases, until the inevitable strikes and, for months, possibly even years, the contingency fee side of the business cases keep demanding more and more money without providing any returns. One little push — like the billable hour side of the business going through a dry spell for a month or two — and the practice goes over the cliff and into bankruptcy.

Which brings us back to those handful of prominent solo practitioners who seem to be making money hand-over-fist with this model. To the extent they’re not in debt up to their eyeballs — and plenty of them are — they are able to do it because their large referral network ensures them far more regular billable hour income, while the big war chest enables them to weather those “black swan” moments when every part of the business seems to be going wrong and they have a catastrophic drawdown.

So what’s the practical message for lawyers thinking about delving into solo practice? That they should be wary of contingency fee work unless they have not just the ability to fund the case, but the ability to fund the cases for years — while also paying their office expenses and themselves — in the event their other revenue dries up or their expenses explode. Young lawyers with a solo practice are probably better off limiting themselves to contingency cases with minimal costs and referring the rest to a firm big enough to utilize the law of large numbers.