Via Overlawyered and TortsProf, I saw that a new law review article came out last week in the Vanderbilt Law Review, “Products Liability and Economic Activity: An Empirical Analysis of Tort Reform’s Impact on Businesses, Employment, and Production” by Joanna Shepherd. As a products-liability lawyer (and an armchair economist), I was excited, so I printed out a copy, sat down with my highlighter, and, unfortunately, didn’t even make it past the third page without gnashing my teeth in frustration:

Specifically, we know surprisingly little about whether products liability law suppresses economic activity, and which, if any, reforms might improve economic conditions.4

This Article provides empirical evidence that addresses this argument. This issue is particularly salient because economic conditions are worse than they have been in decades, yet the cost of the products liability system continues to grow. Consequently, probusiness groups have intensified their demands for tort reform, maintaining that reforms are essential to improving the economy. Hence, it is imperative for lawmakers to know which reforms can help mend current economic conditions. Moreover, the tort system costs American businesses over $150 billion annually.5

4. AM. TORT REFORM ASS’N, supra note 2.

5. TOWERS WATSON, 2010 UPDATE ON U.S. TORT COST TRENDS 7 (2010)

There are two big empirical problems right out of the gate.

First, the Towers Watson report — Shepherd’s sole citation for the assertion that “the tort system costs American businesses over $150 billion annually” — has been repeatedly discredited for inflating its numbers and for relying on secret proprietary data, instead of the industry standard A.M. Best data. Similarly, as I’ve explained before, even if we corrected the numbers, the Towers Watson study still wouldn’t make any sense: the study absurdly refers to every benefit paid to an injured person as a “cost” to society. This would be an accurate analysis if injured persons took their settlement checks and promptly set them on fire.

In reality, as the Coase Theorem makes clear, money paid out in tort liability is not a “cost” to society, it’s just a transfer from one party to another, because the money goes right back into the economy through payments to medical providers and insurers (who subrogated part of the injured person’s claim). The money left after those medical and insurance costs goes towards remedying the insured person’s lost wages, and thus goes to the same healthy economic expenditures as before, like paying for their children’s education, or buying a new house, or putting food on the table. (Before someone claims, “but the lawyer’s fees are a transaction cost,” remember that, in personal injury litigation, the lawyer’s fees are not added to the defendant’s liability, but rather subtracted from the plaintiff’s recovery, and so they do not add to the overall recovery.)

Second, and even more worrisome in a study that purports to make “empirical” arguments, is the lack of any citation at all for Shepherd’s assertion that “the cost of the products liability system continues to grow.” Have the “costs” of our product liability system actually grown relative to the size of the economy? My hunch would be no; as Shepherd admits, since the 1980s, “state after state enacted legislation designed to curb the [fictitious liability insurance] crisis by limiting the scope of liability and damages,” and the federal government has enacted special liability protections for “general aviation aircraft,” “biomaterials suppliers of raw materials and medical-implant component parts,” and “manufacturers, distributors, dealers, and importers of firearms or ammunition.” I’d add to that list of political victories by product liability defendants the increasing adoption of the Third Restatement of Torts (which essentially eliminates strict liability) and the wholesale elimination of claims against generic drug manufacturers.

In short, product liability law has been increasingly favoring defendants for more than a generation, so why should we assume that the cost of the product liability system is growing relative to the economy?

Indeed, the few pieces of empirical evidence we have indicate that liability in general is contracting. Insurance companies’ surpluses — the amount they have left over after paying out claims — have grown much faster than the economy over the past twenty years, jumping from $138 billion in 1990 to $580 billion in 2010. (Source here, relying on A.M. Best’s data.) That surplus indicates that insurers certainly aren’t feeling much of a growth in tort expenses, and that, if anything, they’re charging more than they need to — the insurance industry’s surplus is four times larger than even the grossly inflated “cost” of the whole tort system dreamed up by Towers Watson.

After that worrying opening, the next two-thirds of Shepherd’s article retell the history of product liability law and summarize a variety of anti-consumer reforms (for the full state-by-state list, see this document), then make a bunch of vague assertions that product liability law is no longer needed to make consumers safer. Shepherd asserts, for example, that “Market forces provide a significant incentive for many manufacturers to improve product safety,” as if there were no market forces back in 1965 when Unsafe At Any Speed was published, and as if we still didn’t see wave after wave of hopelessly unsafe products, ranging from rifles that fire with the safety on, to exploding tires, to another 60,000 mesothelioma cases expected over the next few decades.

I was about to give up on Shepherd’s article without having even made it to the empirical analysis, but I’m glad I stuck with it — there are problems with the study, but they’re problems that reinforce one of my longtime arguments on this blog: tort liability has, at most, a trivial impact on the economy.

Shepherd uses “a sophisticated triple-differences methodology” that is “still relatively new in the empirical literature.” In short, focusing on the period from 1977 to 1997, she looked at a couple general indicators of a state’s economy, like GDP, employment, and new small businesses, and then tried to tease out differences between “low-risk” industries that presumably don’t feel the effects of product liability law (e.g., “business services”) and “high-risk” industries at the forefront of product liability law, like manufacturing. Someone has to be the first to try a new method, so I don’t fault her for trying it, but the model must admit two serious limitations.

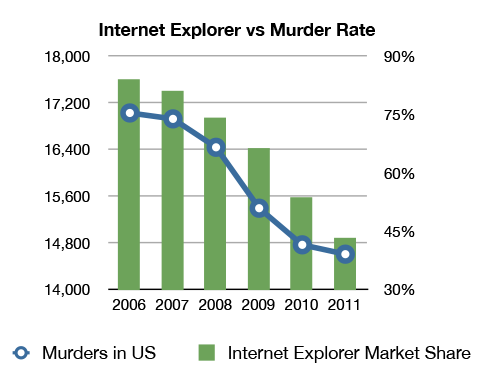

First, Shepherd’s model looks only for correlations, rather than any causal relationship. As shown by the adjacent, hilarious image, the old scientific maxim that ‘correlation does not imply causation’ should always be remembered whenever an economic study tries to “prove” that a certain change in the law caused a certain economic effect. In this case, I think her results ironically show not that tort reform in the area of product liability produces economic benefits, but that product liability law simply doesn’t affect the economy much one way or the other.

First, Shepherd’s model looks only for correlations, rather than any causal relationship. As shown by the adjacent, hilarious image, the old scientific maxim that ‘correlation does not imply causation’ should always be remembered whenever an economic study tries to “prove” that a certain change in the law caused a certain economic effect. In this case, I think her results ironically show not that tort reform in the area of product liability produces economic benefits, but that product liability law simply doesn’t affect the economy much one way or the other.

Shepherd identifies seven main types of product liability “reforms” that she examines:

- Product-Seller Liability [absolving distributors, sellers and retailers of liability for dangerous products]

- Noneconomic Damage Caps

- Eliminating or Limiting Joint and Several Liability [making injured people, rather than profitable companies, eat the loss when one of the defendants goes bankrupt]

- Comparative Negligence [most states have this — the issue is applying it to strict liability]

- Punitive Damage Caps

- Collateral Source Rule Abolishment

- Statute of Repose Limitations [i.e., the latest possible date to sue after a product is sold, regardless of when the injury occurred]

I’ve ranked the above proposals in the order that, in my humble opinion, best reflects how worried plaintiff’s-side product liability lawyers are about them. “Product-Seller Liability” might as well be called “the Walmart law,” because the practical effect of that type of tort reform is that Walmart can sell you a child’s toy loaded with radium and you won’t be able to sue them for it (because they’re merely a “seller”), nor will you be able to sue the brand name listed on the package (because they’re merely a “distributor”), you’ll be stuck chasing some fly-by-night company on the other side of the world that was set up for the purpose of evading liability. Trial lawyers obviously don’t want that.

Last on my list above is the statute of repose, which, according to Shepherd, has more impact on the economy than any other form of tort reform (more on that in a moment). To trial lawyers, however, the statute of repose is usually not an issue in product liability cases. Most states don’t have one, and, in all but a few states, it’s 10 years or longer.

The statute of repose matters in product liability litigation over old airplanes and automobiles — e.g., rollover claims for the second-generation Ford Explorer are now barred in Georgia — but in the vast majority of cases, it’s irrelevant. It’s also the liability restriction least likely to produce any immediate effects in the economy, given its time-delayed nature. In contrast, capping noneconomic damages (#2 on my list, but many would say it should be #1) would have an immediate, severe effect on virtually all claims — like it did in Texas, when caps decimated malpractice lawsuit filings there. (Unsurprisingly, the caps did nothing at all to make medical care cheaper or more widely available in Texas.)

Yet, despite the limited impact of the statute of repose to trial lawyers, guess which “reform” had by far the biggest impact on the economy in Shepherd’s study? She writes, “statutes of repose are associated with approximately a 20.92–25.61 percent increase in employment in manufacturing industries during the sample period.” Wow! It’s like a statute of repose can alone can counteract the effects of globalization and restore all the manufacturing jobs lost over the past decade.

Alas, all we’re seeing is a classic example of correlation does not imply causation. Consider this empirical data: from 1977 to 1997, New York’s economy grew 3.7x, California’s economy grew 4.5x, Texas’ economy grew 4.7x, and Florida’s economy grew 6x. Texas and Florida have statutes of repose, while New York and California do not. Did the statute of repose cause the faster growth in Texas and Florida, or is it coincidental? I think the answer is obvious; the supposed economic benefits of having a statute of repose are merely a mirage, a side-effect of much larger trends at work.

But I think the bigger problem of this whole exercise is the mistaken assumption that liability always amounts to a “cost” on society. Shepherd’s model, like the Towers Watson model, ignores two fundamental facts about the economics of personal injury: when a person is injured, that injury imposes a cost to society, and when a person is not injured, that reflects a savings to society. When a person is injured by a defective product, their medical care and their lost wages are a cost to society created by the defective product, not by the legal liability. Changing product liability law to introduce “reform” doesn’t make those costs go away — if anything, it increases those costs, by removing the incentive to make products safer — it just makes victims, rather than culpable parties, bear the expense of them.